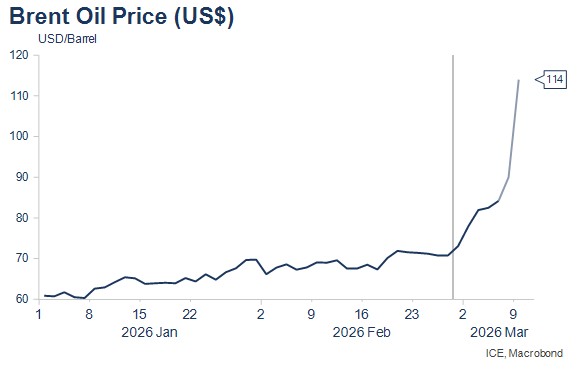

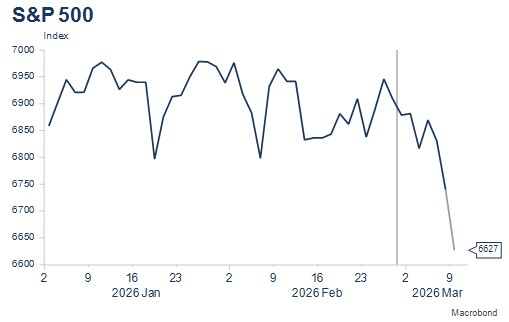

Markets react according to Gulf War 1990 playbook (oil up sharply, equities down and bond yields higher). While Strait of Hormuz closed, oil prices could continue to rise, further pressuring bonds and equities.

Key Points

- Major markets have mostly followed the 1990 Gulf War playbook we covered last week, with spot Brent oil up sharply from around $73pb prior to last weekend’s military action, closing at $90pb on Friday and rising a further $5 in weekend trading on IG Markets. In early Monday trading, prices have surged to $104.50 (43% higher than pre-action levels).

- Share markets only declined modestly last week (-2%), mostly on Friday, though those moves have doubled in early Monday trading on the renewed surge in oil prices.

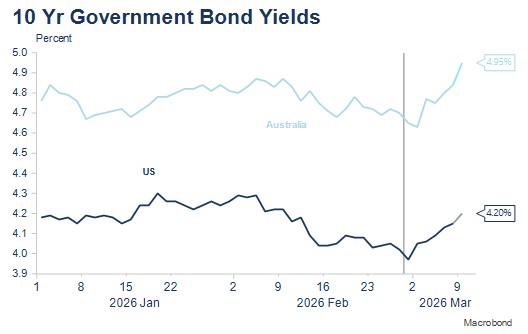

- US and Australian ten-year bond yields rose around 20 basis points last week on inflationary concerns, moves that have been extended by another 5-10 basis points in early Monday Australian trading. These trends were also evident in 1990.

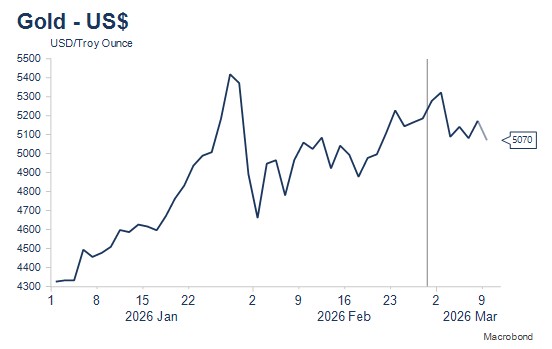

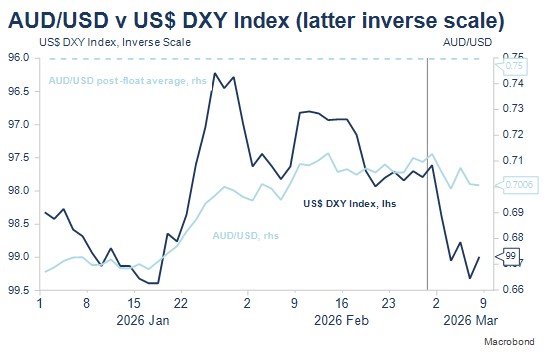

- Expectations of further easing by the Fed have been pushed back and lessened a little since last week, while in Australia, a second interest rate rise is now fully priced by May, a little earlier than last week, though confidence in a move next week has reduced. Gold prices remain high, but eased during the week, perhaps as profits were taken to offset other losses, while the US$ has strengthened modestly (+1.4%). The $A has weakened commensurately and has slipped a little below US$0.70 early in the new week.

- Our conclusion last week based on analysis of the 1990 Gulf War was that central banks will ultimately react to developments in domestic fundamentals. Then, the Australian and US economies were entering recession, unemployment rose sharply, and both central banks eased through the conflict. The current economic backdrop seems a little different, at least for now, with both central banks battling above-target inflation. Inflation will likely move further away from target in the near-term given recent oil price developments, though those movements will also produce a drag on economic growth in the medium term.

- In the short term, the key issues remain the extent to which oil prices rise, how long oil prices remain elevated and the extent to which oil and other energy infrastructure is damaged. The rises in oil and gas prices have been very large given around 20% of global oil and LNG shipments pass through the Strait of Hormuz each day. Further sharp increases could occur while the waterway is effectively closed, but these should be able to quickly reduce if shipping movements can be restored as they are not the same as damage to infrastructure. Both obviously depend on the military course of the conflict. So far, despite US and Israeli military superiority, Iran is exhibiting resistance, which will likely see further oil price gains (and other previously discussed market movements – weaker shares and higher bond yields), while the resistance persists.

- Economic data will therefore again take a back seat to developments in energy markets and the Middle East. The calendars are in any case light, but important in both Australia and the US. There isn’t any central bank speak to worry about as both central banks are in communications blackout ahead of upcoming Board Meetings (Australia, March 16-17) and the US (March 17-18). The economic data support a further tightening in Australia in the very short term, though the market is now only ascribing a 16% chance for this meeting, halving that probability on Monday morning as oil prices surged. No change is widely expected for US rates, with commentary on the labour market key, as well as the number of dissenting voters.

- Except for Australian Consumer Sentiment, data to be released this week pre-dates the Iran conflict. It should therefore be interpreted as providing context for each economy in the event the conflict resolves in a short time. For each day the conflict extends, and the Strait of Hormuz remains closed, higher oil prices and associated market and economic implications will be factored into decision making.

- It’s likely consumer sentiment will show some negative impact as the survey only covers a little of the period of military action. Higher oil prices will add additional pressure to already strained consumer finances, while also acting as a further supply side inflationary shock.

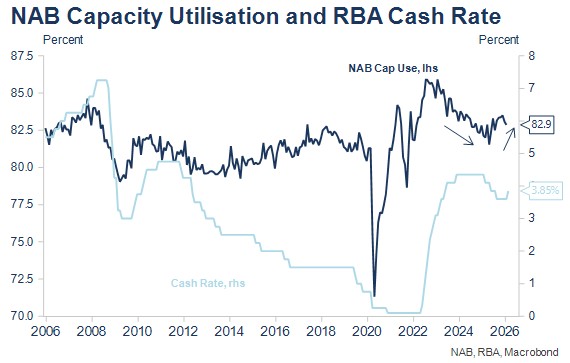

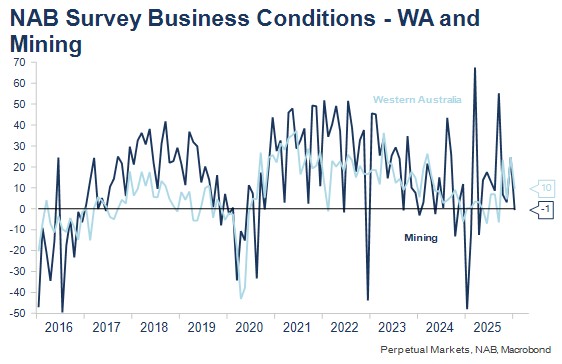

- The NAB Survey capacity utilisation measure should be closely watched, given the RBA’s current narrative about a capacity-constrained Australian economy (not that I fully support that interpretation, believing it’s more about tightness in the labour market). I’ll also be taking a keen interest in business conditions in Mining and WA, which I see as an under-estimated development in supporting Australian activity.

- In the US, there are two readings on inflation published this week – the February CPI on Wednesday and the delayed January PCE deflator on Friday. I’m a little more interested in the delayed January JOLTs reading (also published on Friday) as job openings have been sharply lower in both November and December, and no bounce back would support Governor Waller’s claims that the US labour market is weakening again. Friday night’s payrolls revealed a continuing weak employment creation market (though not as weak as the headline figure of -92K, as cold weather, a short government shutdown and a healthcare strike temporarily reduced around 90,000 jobs). The unemployment rate, despite rising 0.1 percentage points in February, has been broadly stable around 4.4% since September last year.

Middle East developments this past week

Oil, shares and bond yields played out mainly according to the 1990 Gulf War playbook we reviewed last week, following the US and Israeli attack on Iran last weekend. Oil (and gas) prices have risen sharply, likely reflecting the impact of the conflict on the transport of energy through the Strait of Hormuz, rather than the reported significant damage to energy production infrastructure. Around 20% of the global output of crude oil and LNG passes through the Strait of Hormuz daily. Brent oil has risen from $73pb on 27 February to around $90pb at the close on Friday. IG Markets weekend oil prices have recorded a further increase to near $95pb and prices surged to $114 early on Monday.

Share prices have fallen less substantially last week than might have been expected, with the S&P500 only 2% lower than the close the previous Friday. Weekend markets suggested a further 0.75% drop this morning on opening but falls of nearly 4% have occurred given much higher oil prices on Monday.

At the same time, US and Australian ten-year bond yields both rose around 20bps last week and another 10bps in early Australia trading as markets price the potential for higher inflation. That’s problematic for central banks already concerned with above-target inflation rates.

Gold prices however are net a little lower, with the suggestion that after an initial rise on global uncertainty, losses in other markets saw winning gold positions cut to offset these losses. The US$, has strengthened, but like US stocks, only a little, with the $A easing back around 1.25 US cents as the US$ strengthened.

Our analysis last week concluded that central banks ultimately were likely to follow domestic fundamentals as they did in 1990, where rising unemployment due to the onset of recession saw substantial easing enacted. Oil prices exacerbated growth developments, but the recession was caused by very high interest rates and a commercial property bust. Oil prices had unwound much of the Gulf War premium even before Operation Desert Storm had begun.

The economic context this time around in the US is somewhat different, with a boom in AI and defence spending likely leading to less of a drag on growth initially, and inflation rising further away from target in the very near term. Critical, will be the length of time crude prices stay elevated along with the levels to which prices rise. The effects of an extended closure of the Strait of Hormuz will be like the supply chain difficulties experienced during COVID, which was quite an inflationary period, though demand could be expected to be weaker.

The week ahead: Economic Calendar – Key Australian and US events

- Tuesday 10 March – Consumer Sentiment (March); NAB Business Survey (February).

- Wednesday 11 March – AOFM tenders $1bn, 4.25% 2036 bond. (Overnight) US CPI (February).

- Friday 13 March – AOFM tenders $150m 0.25% 2032 Inflation Indexed bond. (Overnight) US PCE (January) and JOLTs (January).

- RBA and US Federal Reserve in communications blackouts ahead of 16-17 and 17-18 March policy meetings, respectively.

One would expect a negative impact on consumer confidence from news of developments in the Middle East, though this will have occurred part way through the survey period. The NAB Business Survey will be closely scrutinised for trends in capacity utilisation, which the RBA has highlighted as a justification for unexpected inflation strength. Capacity utilisation fell back a little in January. I’ll also be very interested to see whether business conditions bounce back from anomalous weaker readings in January for both WA and Mining. The latter was an under-appreciated factor in an improving Australian growth outlook ahead of Middle East developments.

Offshore, with the Fed (and RBA) in blackout, there won’t be Fed speeches to pour over. There are important inflation updates (February CPI on Wednesday and the delayed January PCE on Friday). The delayed January JOLTs data is also released on Friday and is arguably more interesting as ultimately, inflation follows the labour market. Job openings have fallen sharply in the past two months (down nearly 1 million or 12%). Like Job Ads in Australia, it can be difficult seasonally adjusting this data around Christmas time – it’s important that some bounce back occurs otherwise the signal is quite bearish for the labour market and more bullish for interest rates.