Perpetual Markets Economic and Interest Rate Update – Monday 23 February 2026

More tariff uncertainty. January CPI could determine if a follow-up RBA interest rate rise occurs as early as March. Australian labour market remains a little tight.

Key points

- US Supreme Court rejects the method by which President Trump implemented his Liberation Day tariffs. While again confusing, and perhaps a bureaucratic nightmare if companies pursue tariff refunds, one has to expect the end result is limited market impact with the President finding another way to implement his tariff policies. Already, in response, President Trump has introduced a global tariff applying to all countries of 10% and then further increased this to 15%. This of course, is higher than Australia's existing 10% tariff rate.

- It's a light calendar week in the US, with mainly second-tier regional Fed surveys of manufacturing and services published. There are lots of Fed speakers, which will be interesting given last week's FOMC Minutes revealed several members backed a balanced signal on interest rates (suggesting the next move could be either up or down). Despite this, US markets are pricing two interest rate reductions over 2026, but these are well spread out with the first cut not priced until the late July meeting. I remain interested in Waller's thoughts on the labour market as he was early in detecting downside risks to employment and arguing for further easing last year.

- The all-important Australian January monthly CPI is released on Wednesday to the backdrop of another very low unemployment reading of 4.1% for January. Last week's RBA Minutes revealed the Monetary Policy Board viewed employment downside risks as having lessened (tick) and inflationary risks as having risen. That saw the Board conclude that tighter policy was required to return inflation to target. Monthly trimmed mean outcomes averaging just over 0.2% are required to annualise at the midpoint of the RBA's 2-3% target. A 0.3% m/m trimmed mean outcome again seems likely this month, which would still be too high to prevent a follow up rate rise in May. A 0.4% m/m trimmed mean rise would significantly increase the chance of a March interest rate rise.

- Australia also has Construction Work Done and Private New Capex, partial indicators of Q4 GDP, which is released next week. The GDP data is already very dated. Most interest in both series will be the extent to which data centre construction buoys the results.

The week in review

There seems to be no end of news for markets and investors to try to digest! The key developments since our last report on 16 February have been:

- As we start the week, the US Supreme Court has rejected the method by which President Trump implemented his Liberation Day tariffs. While potentially an administrative nightmare if firms are able to obtain refunds for these tariffs, it’s likely the President will simply find another way to implement his tariff and trade policies. Already, he has implemented a 10% global tariff on all countries, which he has subsequently raised to 15% over the weekend.

- The RBA February Board Minutes highlighted that the Board viewed the downside risks to employment as having lessened, while upside risks to inflation had risen. Together, this meant the RBA staff could not forecast a return of inflation to target without tighter monetary policy. There is one further interest rate rise in 2026 incorporated into their February forecasts.

- The unemployment rate surprised to the downside in January, again printing at a very low 4.1%, when a slight retracement of the fall recorded in December was expected.

- The January FOMC Minutes revealed a number of members supported a balanced directive on interest rates, whereby the next move could be either up or down.

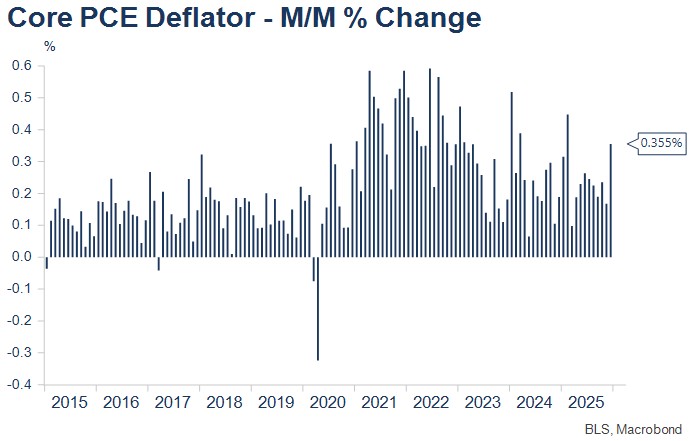

- US core PCE inflation was a stronger than expected 0.36% m/m in January, the largest increase since February last year. PCE inflation needs to average around 0.165% a month to annualise at the Fed’s 2% inflation target.

- Tensions remain high is the Middle East, with ongoing negotiations between the US and Iran accompanied by a significant US military build-up in the region also.

- Considerable uncertainty remains about the ultimate impact of AI on the economy, employment and various parts of the share market. “Software as a Service” companies’ share prices have been significantly impacted in recent months. For me, the ultimate impact of AI on employment remains the number one macro issue for those managing fixed income or interest rate exposures to contemplate.

Recent market movements

There are a huge number of influences currently impacting on markets and investments:

- Australian shorter-term interest rates are mostly reflecting changing views about the extent of likely further tightening required to return inflation to target in a reasonable timeframe. This week’s January CPI previewed later, is very important in this regard.

- Longer-term interest rates are indirectly reflecting a combination of concerns about AI on short-term technology share valuations and longer-term employment impacts.

- Precious metal prices appear to reflect lower US interest rates, a weaker US$ and geopolitical concerns.

- The $A is reflecting both higher Australian interest rates relative to US interest rates and stronger precious metals, base metals and lithium prices.

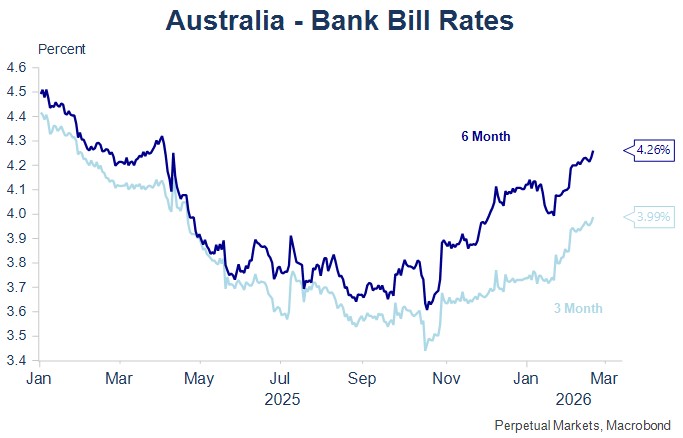

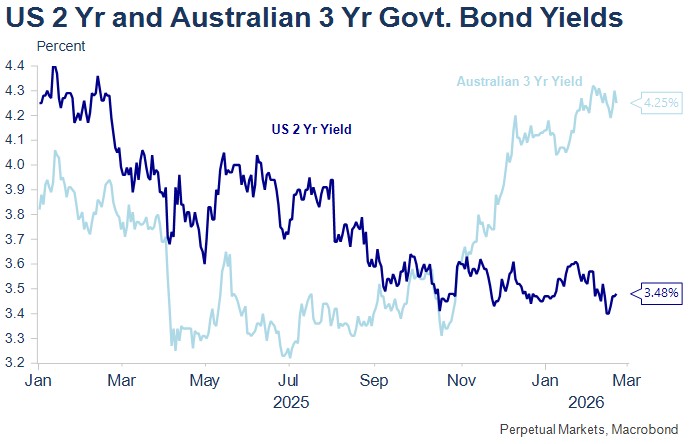

Over the past week, Australian bill rates continued to lift, principally on the back of the stronger than expected Australian January labour market data. The Australian market is now pricing a further 1.4 interest rate increases over 2026, with the next increase almost fully priced by the June Board Meeting.

At the same time, US markets continue to price interest rate cuts, with two further cuts priced in 2026 (one by July and the second by December), and a further half a rate cut in the first half of 2027. FOMC members and the Fed chair have been communicating that an ultimate moderation in US inflation toward target would be sufficient to bring about some further easing, though, it appears that some of this pricing might also reflect ultimate concerns of the impact of AI on the US labour market. The latter will ultimately impact on the Australian economy and interest rates also, though in the short term, higher Australian yields reflect the pricing of the divergent track for the respective central banks.

Australian Labour Market review

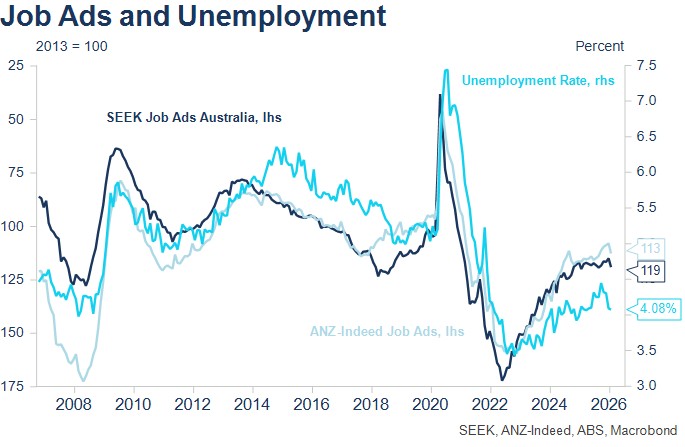

In recent weeks, I have highlighted the importance of labour market indicators. This reflects two themes. First, the labour market provides an important economic bottom line, effectively summing up all the divergent influences. This is extremely important at times like the present when there are large longer-term structural developments interacting with important shorter-term influences. Second, job ads are a very reliable leading indicator of the unemployment rate, which in turn often leads the RBA’s interest rate deliberations.

Last week’s Minutes from the February Board Meeting revealed that the Board increased interest rates as downside risks to employment had lessened, while upside risks to inflation had risen. Together, these developments could not see the staff plausibly forecast a return of inflation to target without more restrictive policy settings.

Developments on both the inflation and unemployment front – the dual mandate the RBA Board has to balance – will determine the extent of further RBA tightening. Last week contained important updates on the labour market on two fronts – SEEK job ads and the official labour market data for January.

The unemployment rate surprised on the low side, once again printing at 4.1% (economists had expected some reversal of the previous month’s 0.2percentage point decline). That’s a pleasingly very low unemployment rate, but also a rate that’s likely to be below the rate considered to be consistent with at-target inflation.

Meanwhile, SEEK job ads increased 3.6% in January, more than doubling the 1.5% fall recorded in December. This data can be very volatile around the Christmas period, but looking more broadly, job advertising has been trending mainly sideways for the past eighteen months. As such, that’s not providing any imminent signal of a substantial increase in the unemployment rate. That will see the RBA continue to conclude that the Australian labour market remains a little tight, and unfortunately for mortgage holders, that short-term interest rates need to rise further to return inflation to target.

Short-term market drivers and the economic calendar this week

It’s a relatively quiet week for US data, though there are plenty of Fed speakers to opine on their views about US monetary policy. As above, while the US Supreme Court ruling is potentially administratively very messy, I’d expect the President to simply find another way to implement his trade and tariff policies, meaning limited overall market impacts.

The key focus will be on Australia’s January monthly CPI release, which has the ability to shift views about the probability of an early follow-up interest rate increase at the RBA’s mid-March Board Meeting. The market is forecasting a 0.3% m/m increase in the trimmed mean, a rate which if sustained through the March quarter, would be broadly consistent with the RBA’s February forecast for a Q1 CPI trimmed mean result of 0.9% q/q. That rate of inflation, however, is unacceptably high relative to the RBA’s directive to target the midpoint of the 2-3% target and would see another interest rate rise enacted relatively soon. A 0.4% monthly increase in the trimmed mean would give the nod to the next rise occurring as early as the March Board Meeting, given the again very low 4.1% unemployment rate recorded in January, which was released last week.

Governor Bullock appears in an evening fireside chat on Wednesday after the CPI, while the RBA’s Head of Economic Analysis, Michael Plumb, addresses the Australian Business Economists’ Annual Forecasting Conference on the topic “Australian Economic Outlook 2026”. That speech is likely to follow the script of the February Statement on Monetary Policy closely.

Economic calendar – key Australian and US events this week

- Monday 23 February – (overnight) Durable Goods Orders (January).

- Tuesday 24 February – “Australian Economic Outlook 2026”, Michael Plumb, Head of Economic Analysis Department, RBA (7.40am); (overnight) President Trump State of the Union Address.

- Wednesday 25 February – CPI (January); Construction Work Done (Q4); RBA Governor fireside chat (7.20pm); (overnight) Nvidia reports.

- Thursday 26 February – Private New Capital Expenditure (Q4), Initial Jobless Claims.

- Friday 27 February – (overnight) US PPI (January).

- Speeches from the Fed’s Waller (Monday), Goolsbee, Collins, Bostic, Waller, Cook, Barkin and Collins (Tuesday), Barkin, Schmid and Musalem (Wednesday).